Alberta vs Ontario Closing Costs: What Ontario Buyers Actually Save | Homes with Tristan

Alberta vs Ontario Closing Costs: What Ontario Buyers Actually Save on a $600K Purchase

One of the most common things I hear from Ontario buyers after they run the numbers on an Edmonton purchase: "I didn't realize how much we were actually saving." The home price difference gets most of the attention. But closing costs, taxes, and the ongoing cost-of-living gap often add up to more than the sticker price spread suggests. Here's the full breakdown on a $600,000 purchase.

These numbers are based on Alberta and Ontario government fee schedules and are accurate as of 2026. They apply to a standard resale purchase, not a new build (GST rules differ on new construction).

- Alberta's land title registration fee on a $600,000 purchase is approximately $484, compared to $8,475 in Ontario and $16,200 in Toronto (provincial plus municipal combined). That single line item is the biggest closing cost difference.

- Total estimated closing costs in Alberta on a $600,000 resale purchase run $3,500 to $5,000, roughly 0.6% to 0.8% of purchase price. In Ontario outside Toronto, expect $11,000 to $13,000. In Toronto, $19,000 to $22,000.

- Alberta's 5% GST vs. Ontario's 13% HST means 8% less tax on everyday purchases. On $2,000/month in taxable spending, that's about $1,920 saved annually.

- First-time buyers in Ontario can claim LTT rebates up to $8,475 combined (provincial plus Toronto), which narrows but doesn't eliminate Alberta's advantage.

What Are Closing Costs in Alberta?

Alberta buyers generally budget 1.5% to 2% of the purchase price for total closing costs on a resale home (Deeded, 2026). That range is significantly lower than Ontario's because Alberta has no provincial land transfer tax. Here's what the line items actually look like on a $600,000 purchase:

| Closing Cost Item | Alberta Estimate | Notes |

|---|---|---|

| Land title registration fee | ~$484 | Based on $600K purchase + $480K mortgage (typical 80% LTV) |

| Real estate lawyer | $1,200 to $1,800 | Varies by firm; most Edmonton lawyers in this range for standard resale |

| Title insurance | $200 to $350 | Lender typically requires; protects against title defects |

| Home inspection | $500 to $650 | Standard for resale; strongly recommended |

| Property tax adjustments | $500 to $1,200 | Depends on possession date and seller's prepayment |

| Total estimate | $2,900 to $4,500 | Roughly 0.5% to 0.75% of purchase price |

No mortgage insurance to calculate here if your down payment is 20% or more. If you're putting less than 20% down, CMHC insurance is added to the mortgage, not paid at closing. It doesn't show up as an out-of-pocket closing cost.

The Land Transfer Tax Difference: The Biggest Number in This Conversation

Ontario's land transfer tax is calculated on a bracket system. On a $600,000 purchase outside Toronto: 0.5% on the first $55,000, 1% on the next $195,000, 1.5% on the next $150,000, and 2% on the remaining $200,000. Total: $8,475 (WOWA.ca, 2026). If you're buying in Toronto, the city adds a mirror tax bringing the combined total to $16,200 on a $600,000 purchase.

Alberta charges a land title registration fee instead. The formula: a $50 base, plus $2 for every $5,000 of purchase price, plus a separate mortgage component. On a $600,000 purchase with an $480,000 mortgage, the combined fee runs approximately $484. That's the entire Alberta equivalent of Ontario's land transfer tax.

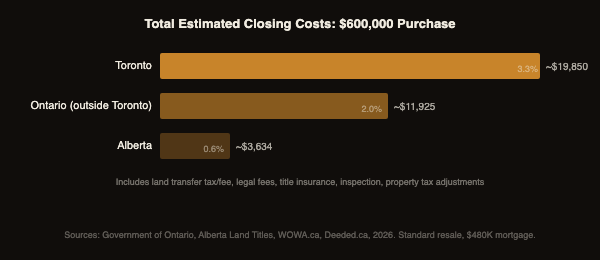

The Full Ontario Closing Cost Picture on $600K

For comparison, here's what a $600,000 purchase looks like in Ontario and in Toronto with the full closing cost stack:

| Item | Alberta | Ontario (non-Toronto) | Toronto |

|---|---|---|---|

| Land transfer tax / registration | ~$484 | $8,475 | $16,200 |

| Real estate lawyer | ~$1,500 | ~$1,800 | ~$2,000 |

| Title insurance | ~$275 | ~$350 | ~$350 |

| Home inspection | ~$575 | ~$500 | ~$500 |

| Property tax adjustments | ~$800 | ~$800 | ~$800 |

| Total estimate | ~$3,634 | ~$11,925 | ~$19,850 |

| Closing costs as % of purchase | ~0.6% | ~2.0% | ~3.3% |

What About First-Time Buyer Rebates in Ontario?

Ontario does offer land transfer tax rebates for first-time buyers. The provincial rebate covers up to $4,000 of the Ontario LTT, and the Toronto municipal rebate adds up to $4,475. Combined maximum: $8,475. For a $600,000 purchase in Toronto, a first-time buyer gets back $8,475, reducing their effective LTT from $16,200 to $7,725 (WOWA.ca, 2026).

That rebate narrows the gap, but doesn't close it. Even with the maximum combined first-time buyer rebate applied, a Toronto first-time buyer on a $600,000 purchase still pays $7,725 in LTT versus Alberta's $484. And the Ontario rebate only applies if you've never owned property anywhere in Canada before, you're a Canadian citizen or permanent resident, and the home is your principal residence. It also only applies once.

Alberta has no LTT at all: no rebate needed because there's no tax to rebate.

The Ongoing Tax Advantage: Sales Tax, Income Tax, and Health Premiums

The closing cost difference is a one-time event. The ongoing cost differences compound every year after the move. Alberta's 5% GST applies to most everyday purchases versus Ontario's 13% HST. That 8% gap on $2,000 per month in typical taxable spending adds up to about $1,920 annually (Make Your Move Calgary, 2026).

Alberta also doesn't charge the Ontario Health Premium, which costs Ontario residents between $300 and $900 per year depending on income. And Alberta introduced a new 8% provincial income tax bracket in 2025 that saves individuals up to $750 per year compared to the previous rate.

Put the one-time and annual numbers together: a buyer moving from Toronto to Edmonton on a $600,000 purchase saves roughly $15,716 on closing day alone. Add $1,920 in annual sales tax savings plus up to $1,650 in other provincial tax savings, and the first year financial advantage clears $19,000. Over five years, that's well over $25,000 beyond the home price gap. This is what most Ontario buyers aren't accounting for when they do their initial math.

What to Actually Budget for Closing in Alberta

For an Edmonton purchase in the $500,000 to $750,000 range, I tell buyers to set aside $4,000 to $5,500 for closing costs. That covers the land title fee, legal fees, title insurance, home inspection, and a buffer for property tax adjustments and any other small items that come up. If you're putting less than 20% down, add CMHC insurance to your mortgage calculation (but not to your closing cost cash).

The rule of thumb I use with out-of-province buyers: budget 1% of the purchase price for closing costs and you'll be comfortable. Anything left over on closing day is yours to keep for moving costs or early home expenses. See the full Ontario buyer mistake guide for context on why pre-approval and deposit setup need to come first.

Want the full financial picture before you buy?

I walk every out-of-province buyer through a full cost comparison before we start looking. Let's make sure the numbers actually work for you.

Book a 15-Minute CallFrequently Asked Questions

Does Alberta have a land transfer tax?

No. Alberta charges a land title registration fee instead, which is a flat government charge based on the purchase price and mortgage amount, not a percentage-based tax. On a $600,000 purchase with an $480,000 mortgage, the total registration fee is approximately $484, compared to $8,475 in Ontario outside Toronto.

How much should I budget for closing costs in Alberta?

Budget 1% of the purchase price and you'll be comfortable. On a $600,000 home that's $6,000, which covers land title fees, legal fees, title insurance, home inspection, and adjustments with room to spare. Real closing costs typically run $3,500 to $5,500, so 1% gives you a reasonable buffer.

Do I pay GST on a resale home in Alberta?

No. GST applies to new construction homes, not resale. If you're buying a previously-owned home in Edmonton or Sherwood Park, there is no GST on the purchase price. GST does apply to real estate commissions, legal fees, and other services associated with the transaction, but not the property itself.

What is the Ontario first-time buyer land transfer tax rebate?

Ontario refunds up to $4,000 of the provincial LTT for eligible first-time buyers. Toronto adds a separate municipal rebate of up to $4,475. The combined maximum is $8,475. Eligibility requires that you've never owned property anywhere in Canada before, you're a Canadian citizen or permanent resident, and the home will be your principal residence.

Is property tax lower in Edmonton than Ontario?

It depends on the municipality and assessment. Edmonton's residential mill rate and Sherwood Park's are generally competitive with mid-sized Ontario cities, though lower than Toronto. On a $600,000 Edmonton home, annual property tax typically runs $3,500 to $5,000. The bigger ongoing financial advantage is the absence of provincial sales tax, not the property tax rate.

Categories

Recent Posts