Acreage Mortgages in Alberta: The Rules That Catch Buyers Off Guard

Homes with Tristan: Alberta Buyer Finance

Acreage Mortgages in Alberta: The Rules That Catch Buyers Off Guard

By Tristan Boire, REALTOR | Park Realty, Sherwood Park AB | June 1, 2026

Most buyers who start looking at acreages near Edmonton do the obvious math: purchase price, estimated mortgage payment, done. What they miss is everything around the mortgage, and the ways the mortgage itself works differently on a rural property. By the time some of them realize it, they're already under contract.

This post breaks down the actual financing picture for acreage buyers in Alberta in 2026: the CMHC rules that apply differently to rural properties, why lenders often ask for more than the minimum down payment, what rural insurance actually costs, and what your true monthly carrying cost looks like on a $1M acreage versus a comparable city home. Get comfortable with these numbers before you start looking.

Key Takeaways

- →For a $1M acreage, the minimum insured down payment is $75,000 (5% on first $500K + 10% on remaining $500K), but many lenders ask for 20–25% on rural properties. Budget accordingly. (CMHC, 2026)

- →Rural insurance, propane heating, and per-structure coverage add $500–$800/month to acreage carrying costs compared to a city home in the same price range.

- →One offset: rural property taxes in Alberta are generally lower than Edmonton city property taxes. Strathcona County runs approximately $200–$300/month less than a comparable Edmonton city address.

How Does the Down Payment Work on an Acreage?

Canada's standard down payment rules apply to most residential acreages: 5% on the first $500,000 of the purchase price, plus 10% on anything from $500,000 to $1,499,999. Above $1.5 million, CMHC mortgage insurance isn't available at all, and you need a full 20% down. On a $1,000,000 acreage, that means a minimum insured down payment of $75,000 (CMHC, 2026).

Here's the catch. "Minimum" and "what lenders will actually approve" are two different things on rural properties. Because acreages are less liquid than city homes, because they can take longer to sell if the bank ever needs to recover the asset, many lenders apply additional scrutiny. It's common for lenders to request 20 to 25% down even when the property technically qualifies for high-ratio insurance. If your pre-approval was based on 10% down and you fall in love with an acreage, you may discover you need significantly more. Have that conversation with your mortgage broker specifically about rural property before you start looking.

There's also the farm property exception. If an acreage resembles a working farm, meaning crops are being grown or animals are being raised on the property, CMHC may treat it as an agricultural property and require a 50% down payment. For most residential acreages near Edmonton, this isn't an issue. But if you're looking at a property with outbuildings that have been used for livestock, or land that's been leased for hay, confirm with your broker before assuming standard rules apply.

Canada's minimum insured down payment on a $1M property is $75,000 (5% on first $500K plus 10% on the next $500K), per CMHC 2026 rules. For rural and acreage properties specifically, many lenders require 20–25% due to lower liquidity and longer average selling timelines compared to urban homes. Properties resembling active farms may require 50% down. Always confirm rural property rules with your mortgage broker before pre-approving. (CMHC, 2026)

What Does Rural Property Insurance Actually Cost?

Rural property insurance costs more than city insurance, and it's not a small difference. Three factors drive the premium: distance from fire services, the number of structures on the property, and specialized coverage requirements for well/cistern and septic systems.

Distance from fire services is the biggest single driver. City homes are minutes from a fire hydrant and a fire station. An acreage 20 minutes from Sherwood Park has a meaningfully longer emergency response time, and the insurer prices that risk. This alone can push your annual premium $500 to $1,500 higher than a comparable city policy.

The per-structure rule catches a lot of buyers. In Edmonton, your policy covers the house and typically a garage. On an acreage, every insurable structure needs to be listed: the shop, any outbuilding, a barn, a storage structure. They don't insure themselves by default. If a shop burns down that wasn't on the policy, the insurer pays nothing for it. Make sure your broker lists every structure when quoting. And if you add a structure after the policy is written, call your broker the same week.

Cistern and septic coverage is a separate line item most city insurance brokers aren't used to writing. It covers the cost of a cistern failure, a septic backup, or a well contamination event. On a property with municipal water and sewer, you don't need this. On an acreage, you do. Get an explicit quote that includes it.

Rural property insurance in Alberta costs more than city insurance for three reasons: longer fire response times (higher risk premium), per-structure coverage requirements for shops and outbuildings, and specialized cistern/septic system riders that don't exist on city policies. Buyers should get an insurance quote before finalizing their acreage budget, not after. Annual premiums on a $1M acreage property can run $1,000–$2,000 more than a comparable Edmonton city home. (Cornerstone Insurance, Edmonton, 2026)

The Heating and Utility Variables Nobody Mentions

This is the one that surprises buyers most often. Acreages don't always have natural gas. Many run on propane. Natural gas and propane are both hydrocarbons, but they're priced very differently. Natural gas is billed by the GJ (gigajoule) and delivered by pipeline. Propane is delivered by truck, stored in an on-site tank, and billed by the litre. At Alberta's current propane prices, a home that costs $180/month to heat on natural gas can cost $300 to $400/month on propane for the same square footage and climate zone.

Why does it matter for your mortgage calculation? It doesn't directly affect the mortgage itself. But it affects your debt service ratios if your lender is calculating total monthly housing costs, and it absolutely affects your monthly budget. Ask the seller's agent whether the property is on gas or propane, and request the past 12 months of heating bills if you're seriously considering it.

The one pleasant surprise on acreage costs: property taxes. Strathcona County property tax rates are lower than City of Edmonton rates because rural municipalities provide fewer urban services. On a $1M acreage in Strathcona County, you might pay $3,200 to $3,600 per year in property tax. A comparable $1M Edmonton city property could run $5,000 to $5,500. That's roughly $150 to $200/month cheaper, and it partially offsets the higher insurance and utility costs.

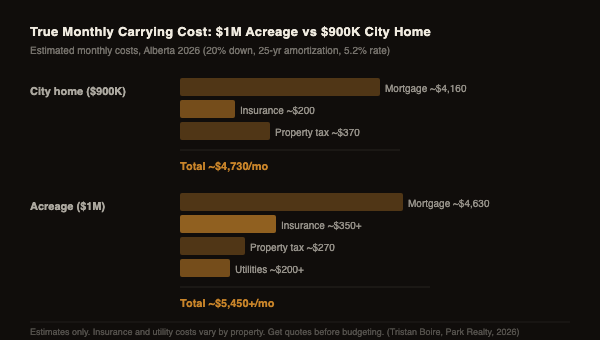

What Does a $1M Acreage Actually Cost Per Month?

Here's a realistic breakdown for a $1M Strathcona County acreage purchased with 20% down ($200,000), at a 5.2% 5-year fixed rate, 25-year amortization in 2026. These are estimates. Every property is different. Use this as a starting frame, then get actual quotes.

| Cost Item | Monthly (est.) |

|---|---|

| Mortgage ($800K, 5.2%, 25yr) | ~$4,800 |

| Rural property insurance | $290–$420 |

| Property tax (Strathcona County) | ~$280 |

| Heating (gas) or propane | $150–$380 |

| Cistern/well + septic maintenance | ~$40 |

| Total (estimated range) | $5,560–$5,920 |

For context, a $900,000 Edmonton city home with 20% down runs approximately $4,700 to $5,200 per month including mortgage, city insurance, and property tax. The acreage runs $400 to $700 more per month on average, depending almost entirely on whether it has natural gas or propane. That's meaningful but it's not a dealbreaker, and the lifestyle and space you're getting in return is the whole point.

Want to run the actual numbers for a specific property? That's exactly the kind of conversation I have with acreage buyers before we start looking. It takes 20 minutes and it means you're shopping with a real budget, not an assumption.

Ready to Run Your Numbers?

Get Your Free Edmonton Buyer Guide

Includes a full buying cost breakdown for Alberta including the numbers city buyers from Ontario and BC always miss.

Download the Buyer GuideFrequently Asked Questions

What is the minimum down payment for a $1M acreage in Alberta?

Under CMHC 2026 rules, the minimum insured down payment on a $1M property is $75,000 (5% on first $500K plus 10% on remaining $500K). However, for rural acreage properties, many lenders request 20–25% due to lower liquidity. Talk to your broker specifically about rural property before assuming standard rules apply.

Is CMHC mortgage insurance available for acreages in Alberta?

Yes, for most residential acreages under $1.5M that are not operating as farms. Properties that resemble working farms (crops, livestock) may require 50% down under CMHC agricultural rules. A standard residential acreage with a shop, landscaping, and no active agricultural use typically qualifies for insured financing.

Are property taxes lower on acreages than in Edmonton?

Generally yes. Strathcona County and Parkland County property tax rates are lower than City of Edmonton rates because rural municipalities deliver fewer urban services. A $1M Strathcona County acreage might pay $3,200–$3,600/year in property tax versus $5,000–$5,500 for a comparable Edmonton address.

What are the closing costs on an acreage in Alberta?

Alberta has no provincial land transfer tax, which is a significant saving versus Ontario. Closing costs typically include legal fees ($1,500–$2,500), title insurance (~$300), home inspection ($500–$650), cistern/well inspection ($350–$600), and septic inspection ($300–$500). Budget 1.5–2% of purchase price total for closing costs on an acreage deal.

How much does propane heating cost on an Alberta acreage versus natural gas?

At 2026 Alberta energy prices, a home that costs $150–$200/month to heat on natural gas can cost $280–$400/month on propane for the same square footage. The gap is significant over a full Alberta heating season. Always confirm the heating source before making an offer and request past utility bills for a realistic monthly estimate.

Keep Reading

Categories

Recent Posts