RRSP Home Buyers Plan in Alberta: How to Use It and What It Actually Costs You

RRSP Home Buyers' Plan in Alberta: How to Use It and What It Actually Costs You

The RRSP Home Buyers' Plan lets first-time buyers in Canada withdraw money from their RRSP to use toward a home purchase without paying income tax on the withdrawal. As of April 2024, the withdrawal limit increased from $35,000 to $60,000 per person. If you're buying with a partner, that's $120,000 combined available from your RRSPs, tax-free, as a zero-interest loan you repay to yourself.

In Alberta, where there's no provincial land transfer tax and the average detached home sat at $604,744 in May 2026 (REALTORS Association of Edmonton, 2026), the HBP can meaningfully change what your down payment looks like. But it comes with specific rules, and the repayment side trips people up more than any other part of it. This post walks through how it actually works.

- The HBP withdrawal limit increased to $60,000 per person in April 2024, up from $35,000. Couples can access up to $120,000 combined (Canada Revenue Agency, 2024)

- Repayment is 1/15th of the total withdrawal per year over 15 years. On a $60,000 withdrawal, that's $4,000/year minimum, or it gets added to your taxable income

- RRSP contributions must be on deposit for at least 90 days before withdrawal, making timing critical for buyers on a shorter timeline

- Alberta has no provincial land transfer tax, so HBP funds go entirely toward the down payment rather than covering a tax bill at close

What the RRSP Home Buyers' Plan Actually Is

The Home Buyers' Plan is a federal program that lets you borrow from your own RRSP to fund a home purchase. Normally, withdrawing from an RRSP creates a tax liability because those funds were contributed pre-tax. The HBP sidesteps that by treating the withdrawal as a loan rather than income, provided you repay it over the required period. You're not spending the money. You're temporarily relocating it from your retirement account into your home.

To qualify, you need to be a first-time buyer, meaning you haven't owned a home that you lived in as your principal place of residence in the past four calendar years. You also need a signed purchase agreement for a qualifying home. The funds must be used to buy or build a home before October 1 of the year following the withdrawal.

The $60,000 Limit: What Changed in 2024

Before April 16, 2024, the maximum HBP withdrawal was $35,000 per person. The 2024 federal budget raised that limit to $60,000, a 71% increase. This applies to all withdrawals made on or after April 16, 2024. Withdrawals made before that date remain subject to the old $35,000 cap.

For a couple buying together, both partners can use the HBP independently from their own RRSPs. That means $60,000 each, for a combined $120,000 available toward the down payment. On a $600,000 home, a $120,000 HBP contribution covers 20%, which is the threshold that eliminates mortgage default insurance (CMHC insurance). That changes the monthly payment and the total cost of the mortgage meaningfully.

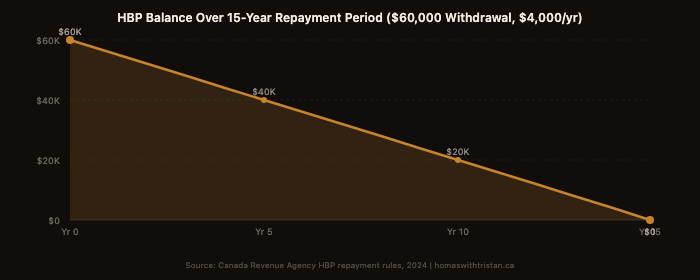

How Repayment Works: The Part Nobody Explains Clearly

Repayment is where the HBP catches people off guard. If you withdraw $60,000, you must repay 1/15th of that amount, or $4,000, to your RRSP each year. The repayment period is 15 years. If you don't make the minimum annual repayment in any given year, that year's required amount gets added to your taxable income for that year. It's not a penalty. It's simply treated as income, which means it's taxed at your marginal rate.

Repayment normally starts in the second calendar year after the year you made your first withdrawal. So if you withdrew in 2026, your first required repayment year is 2028. However, for withdrawals made between January 1, 2022 and December 31, 2025, the federal government introduced a temporary grace period: repayment doesn't start until the fifth year after the withdrawal. A 2024 withdrawal under this window doesn't require any repayment until 2029.

You can repay more than the minimum in any year. Making larger contributions early in the repayment period reduces your outstanding balance faster and frees up RRSP contribution room sooner. There's no penalty for overpaying.

Repayment schedule on a $60,000 withdrawal

| Repayment Year | Annual Minimum | Remaining Balance |

|---|---|---|

| Year 1 | $4,000 | $56,000 |

| Year 3 | $4,000 | $48,000 |

| Year 5 | $4,000 | $40,000 |

| Year 10 | $4,000 | $20,000 |

| Year 15 | $4,000 | $0 |

The 90-Day Rule: The One That Trips People Up

Before you can withdraw from your RRSP under the HBP, the funds must have been sitting in the account for at least 90 days. If you contribute money to your RRSP today specifically to use for the HBP, that money can't be withdrawn for 90 days. You also can't use that contribution for an RRSP tax deduction on your return and then withdraw it for the HBP in the same tax cycle. CRA watches for this.

If you're planning to use the HBP, the practical advice is to have the contributions in place well before you start your active home search. Six months of lead time is reasonable. If you're only starting to think about this now and you haven't made contributions, start immediately, confirm the 90-day clock, and plan your possession date accordingly.

What $60,000 Actually Gets You in Edmonton

Edmonton's detached home average hit $604,744 in May 2026, up 4.3% year-over-year (REALTORS Association of Edmonton, 2026). A $60,000 HBP withdrawal represents about 10% of that average price. For a couple both withdrawing the maximum, $120,000 covers 20% of a $600,000 home, eliminating CMHC insurance and reducing the total mortgage cost.

Alberta's no provincial land transfer tax position matters here in a way that doesn't get discussed enough. In Ontario, a buyer purchasing a $600,000 home outside Toronto pays roughly $8,475 in provincial land transfer tax. In Toronto, add another $8,475 for the municipal LTT. That's money out of the down payment budget before a single dollar goes toward the home's equity. In Alberta, that cost doesn't exist. Your HBP funds go directly toward the purchase, not toward a tax bill.

When Ontario buyers relocating to Edmonton ask me whether their RRSP savings stretch further here, the honest answer is yes, and the LTT savings are a significant part of why. The $16,000-plus that an Ontario buyer would lose to land transfer tax on a $600K purchase can instead sit in the down payment in Alberta. That's not a small number.

Should You Use the HBP?

The HBP makes sense when the tax-free withdrawal allows you to reach a down payment threshold you couldn't otherwise hit, specifically the 20% threshold that eliminates CMHC insurance. The insurance premium on an insured mortgage at 5% down on a $600,000 purchase is $22,800 (4.00% of the $570,000 insured mortgage), added to the mortgage principal. If using your RRSP gets you from 5% to 20%, the insurance premium saving alone may justify the repayment commitment.

It doesn't make sense if your RRSP is generating returns that significantly outpace your mortgage interest rate. Withdrawing from a high-performing investment to avoid a low-rate mortgage cost can leave you worse off over 15 years. This is a calculation worth doing with a mortgage broker or financial planner, not a rule that applies universally.

The repayment obligation is real. For 15 years, you need to contribute $4,000 minimum per year to your RRSP specifically as an HBP repayment. If your income fluctuates or your RRSP contribution room is limited for other reasons, that obligation can become a constraint. Know what you're committing to before you withdraw.

Have questions about your Edmonton buying budget?

HBP, FHSA, closing costs, mortgage math: I'll connect you with the right mortgage broker and walk through the numbers with you before you start your search.

Book a 15-Minute CallFrequently Asked Questions

What is the RRSP Home Buyers' Plan limit in 2026?

The limit is $60,000 per person, increased from $35,000 as of April 16, 2024 (Canada Revenue Agency, 2024). Couples buying together can each use their own RRSP independently, for a combined maximum of $120,000.

How do I repay the HBP without penalties?

Contribute at least 1/15th of your total withdrawal (minimum $4,000/year on a $60K withdrawal) to your RRSP each year, designating it as an HBP repayment on your tax return using CRA Schedule 7. If you miss a year, that amount is added to taxable income for that year, not charged as a penalty.

Can I use both the FHSA and the RRSP HBP for the same purchase?

Yes. The FHSA (First Home Savings Account) and the HBP can both be used toward the same qualifying home purchase. They are separate programs with separate rules. Many first-time buyers in Alberta use both together to maximize their down payment.

Is there land transfer tax in Alberta that would eat into my HBP funds?

No. Alberta has no provincial land transfer tax. The only comparable fee is a land title transfer fee, which is substantially lower (under $1,000 on most transactions). Your HBP funds go toward the down payment, not a tax bill at closing.

What happens if I withdraw RRSP funds and then don't buy a home?

You must recontribute the withdrawn amount to your RRSP by December 31 of the second calendar year following the year of withdrawal, or the full withdrawal amount is included in your taxable income for that year. There is no HBP grace period for buyers who don't complete a purchase.

The HBP is one of the more useful tools available to Alberta first-time buyers right now. The $60,000 limit, the no-LTT environment, and the ability to combine it with the FHSA means the down payment picture has genuinely improved for buyers who've been building RRSP savings. If you want to map out how this looks on an actual Edmonton purchase, I'm happy to connect you with a mortgage broker and work through the numbers together.

Categories

Recent Posts