The $700K Mortgage in Alberta: Monthly Payments, Stress Test, and Income Required in 2026 | Homes with Tristan

Homes with Tristan: Alberta Buyer Finance

The $700K Mortgage in Alberta: What You'll Pay Monthly and What You Need to Qualify

By Tristan Boire, REALTOR | Park Realty, Sherwood Park AB | May 25, 2026

People come to Edmonton with a budget in mind. Seven hundred thousand dollars is a common one right now, especially for families moving from Ontario or BC. The Saturday breakdown covered what $700K buys across different Edmonton neighbourhoods. This post is about the other side: what $700K actually costs to carry, what income you need to qualify, and how to think about the down payment.

Mortgage math matters. Getting the numbers wrong before you start your search wastes everyone's time, including yours. Let's go through it clearly.

Key Takeaways

- →20% down ($140K) on a $700K purchase means a $560K mortgage and no CMHC insurance premium

- →Monthly P&I on $560K at 5% (25yr) is approximately $3,071 using Canadian semi-annual compounding

- →Stress-tested at 7% (5% + 2%), a household needs approximately $160K+ income to qualify (GDS rule, 32%)

- →A couple using both FHSA ($40K each) and RRSP Home Buyers' Plan ($35K each) could access up to $150K combined for their down payment

How Much Down Payment Do You Need on $700K?

For homes priced above $500K and under $999,999, Canada's minimum down payment rules work in two tiers. You need 5% on the first $500K ($25,000) and 10% on the remaining $200K ($20,000). That adds up to a minimum of $45,000. (OSFI guidelines, 2026)

Going with the minimum has a real cost attached: CMHC mortgage insurance. At minimum down ($45,000 on a $700K purchase), the insured mortgage is $655,000. CMHC's premium at that LTV is 4.00%, adding $26,200 to your mortgage balance. (CMHC, 2026) That amount gets rolled into your mortgage, meaning you pay interest on it for the life of the loan.

The 20% threshold is at $140,000. Cross it and the CMHC premium disappears entirely. Your mortgage balance is $560,000 and you're not paying insurance. Most buyers in the $700K range target this if they can get there.

Using FHSA and RRSP to Build the Down Payment

First-time buyers in Alberta have two major registered accounts worth using before buying. The FHSA (First Home Savings Account) lets you contribute up to $8,000 per year to a lifetime max of $40,000. Contributions are tax-deductible and withdrawals for a qualifying home purchase are tax-free. That's as good as it gets from a tax efficiency perspective. (CRA, 2026)

The RRSP Home Buyers' Plan lets each buyer pull up to $35,000 from their RRSP, tax-free at withdrawal, to be repaid over 15 years. A couple buying together can each use $35,000 for a combined $70,000.

In practice, I see a lot of buyers using a combination of both. FHSA first for the tax deduction on contributions, RRSP HBP on top of that, and then personal savings for the gap. A couple who started FHSA contributions two to three years ago and has been maxing both their RRSPs can often hit the $140K threshold from registered funds alone, without touching non-registered savings.

A couple who each max out their FHSA ($40,000 per person) and each access the RRSP Home Buyers' Plan ($35,000 per person) can combine up to $150,000 toward a down payment using registered, tax-advantaged funds (CRA, 2026). On a $700K purchase, that meets the 20% threshold and eliminates CMHC insurance entirely.

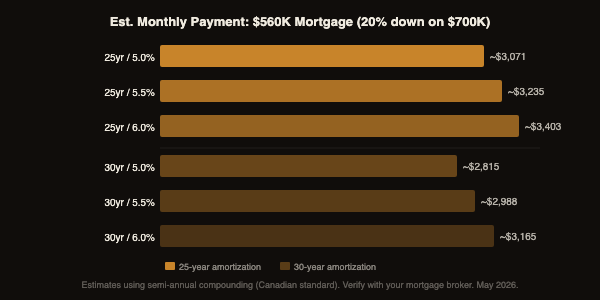

What Monthly Payment Can You Expect?

With 20% down, the mortgage is $560,000. Monthly principal and interest payments depend on your rate and amortization period. At 5% and a 25-year amortization, using Canadian semi-annual compounding, the payment comes to approximately $3,071 per month. At 5.5% it's around $3,235. At 6% it rises to about $3,403. (All estimates. Confirm with your mortgage broker using your actual rate and terms.)

A 30-year amortization lowers the monthly payment by roughly $250–$300, down to the $2,800–$3,200 range depending on rate. But it extends the time you're paying interest, so total interest paid over the life of the loan is meaningfully higher. In a rising equity market like Edmonton's, the lower monthly cash flow can be worth it. In a flat or declining market, extending amortization is more expensive than it looks.

What Income Do You Need to Qualify? (The Stress Test)

Canada's mortgage stress test requires you to qualify at the higher of your contract rate plus 2%, or 5.25%. If you're getting a rate of 5%, you'll need to prove you can handle 7%. The lender isn't expecting you to pay 7%. They just need to know you'd survive it. (OSFI B-20 guidelines, 2026)

At 7% on a $560,000 mortgage over 25 years, the qualifying payment is approximately $3,920 per month. Lenders typically cap your Gross Debt Service (GDS) ratio at 32%, meaning housing costs including mortgage, property tax, and heat shouldn't exceed 32% of your gross income.

Running the numbers: monthly mortgage at qualifying rate (~$3,920) plus property tax (~$443/mo on a $700K Edmonton home, based on the City of Edmonton's 2026 residential mill rate of 0.76%) plus heat estimate (~$150/mo) totals approximately $4,513 in monthly housing costs. Divide by 0.32 and you need roughly $14,100 gross monthly income, or about $169,000 annually.

For a couple, this splits more easily. Two incomes of $84,000 each hits that threshold. Two incomes at $75,000 and $95,000 also works. What lenders look at is the household total, not how it's divided between two earners.

Canada's stress test (OSFI B-20) requires buyers to qualify at their contract rate plus 2% or 5.25%, whichever is higher. On a $700K Alberta purchase with 20% down, buyers qualifying at a 5% contract rate need to demonstrate serviceability at 7%. With Edmonton property tax included in the GDS calculation, the approximate household income required is $160,000–$170,000 annually.

What's the Total Monthly Cost of Owning a $700K Edmonton Home?

The mortgage payment is the biggest number, but it's not the only one. Here's a realistic all-in monthly estimate for a $700K Edmonton home with 20% down at 5% (25-year amortization):

- Mortgage P&I~$3,071/mo

- Property tax~$443/mo (~$5,320/yr using Edmonton's 0.76% residential mill rate, City of Edmonton 2026)

- Home insurance~$175/mo (varies significantly by home and insurer)

- Utilities~$280/mo (gas heating in Edmonton is a real cost, especially winter)

- Total est.~$3,950–$4,200/mo all-in

That's a meaningful number. But compared to Toronto, where $700K likely gets you a condo at a similar or higher monthly cost with strata fees included, the value ratio is completely different. In Edmonton you're owning a detached home with no condo fees and a yard.

One thing I tell people: budget for an emergency fund on top of the monthly carrying cost. Detached homes need maintenance that condos don't. New furnace, roof, water heater. These are real costs. Typically 1% of the home's value per year is a reasonable reserve estimate, which on a $700K home is about $7,000 annually or $580/month set aside.

Ready to Run Your Numbers?

Get the Edmonton Budget Buyer's Guide

Includes a full breakdown of what your budget gets you in Edmonton, closing cost estimates, and a step-by-step walkthrough of the Alberta buying process.

Get the Free GuideFrequently Asked Questions

What is the minimum down payment on a $700K home in Canada?

For a $700K home: 5% on the first $500K ($25,000) plus 10% on the remaining $200K ($20,000), totalling $45,000 minimum. This applies to homes under $999,999. CMHC insurance is required on any mortgage with less than 20% down. (OSFI, 2026)

What income do I need to qualify for a $700K home in Alberta?

With 20% down and stress-tested at 7% (5% rate + 2%), you need approximately $160,000–$170,000 household gross income using the 32% GDS rule with Edmonton property tax included. Couples can combine incomes. Exact qualification depends on other debts, lender-specific criteria, and your actual rate. Speak with a mortgage broker for your specific numbers.

Can I use my RRSP for a $700K home purchase in Alberta?

Yes. The RRSP Home Buyers' Plan lets first-time buyers withdraw up to $35,000 each ($70,000 for a couple) tax-free for a qualifying home purchase. The amount must be repaid over 15 years. Combined with the FHSA ($40,000 lifetime per person), a couple can access up to $150,000 from registered accounts. (CRA, 2026)

Is it better to do 25-year or 30-year amortization on a $700K home?

25 years saves significantly on total interest. 30 years reduces the monthly payment by $250–$300 but you pay interest for an extra 5 years. If cash flow is tight, 30 years improves flexibility. If you can swing 25 years comfortably, the total cost of ownership is lower. Some buyers do 30-year amortization but make accelerated payments when possible.

Does Alberta have any provincial mortgage assistance programs?

As of 2026, Alberta does not have a provincial first-time buyer rebate comparable to Ontario's LTT rebate. However, Alberta has no provincial land transfer tax (only a small land title transfer fee of ~$484 on a $700K purchase), which is effectively a large built-in saving compared to Ontario buyers. Federal programs like FHSA and RRSP HBP apply nationally. Alberta has no additional provincial first-time buyer grants or rebates as of 2026.

Categories

Recent Posts