Is 2026 a Good Time to Buy a Home in Edmonton?

Is 2026 a Good Time to Buy a Home in Edmonton?

The average detached home in Edmonton was $571,372 in February 2026. To anyone coming from Toronto or Vancouver, that number looks like a typo. Whether it’s the right time for you to buy has less to do with the market and more to do with where you stand financially — but the Edmonton market itself is in a reasonable spot right now, and I want to walk through what that actually looks like.

- Edmonton’s average detached home was $571,372 in February 2026 — less than half the Toronto benchmark

- Alberta has no provincial land transfer tax — you save $10,000–$20,000+ at closing compared to Ontario on the same purchase

- Inventory has grown from 2024 levels, giving buyers more selection and more room to negotiate

- The stress test still applies — you qualify at your contract rate plus 2%, so get pre-approved before you start shopping

What Edmonton Home Prices Actually Look Like Right Now

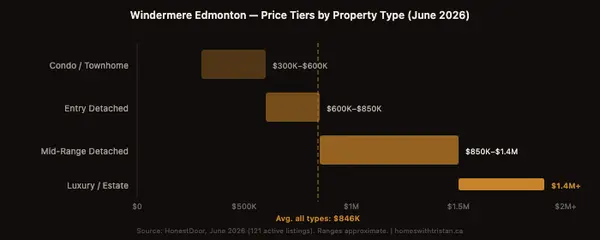

The $571,372 average covers a wide range. Entry-level detached in southwest communities like Glenridding and Keswick starts around $550,000–$650,000. Mature neighbourhoods like Windermere average closer to $1.6M, and Glenora sits around $1.7M. So depending on what you’re looking for, you’re working within a pretty different set of numbers.

Prices have moved from where they were a few years ago. But relative to where most of my clients are coming from — Ontario and BC — Edmonton is still a different category entirely.

| City | Avg. Detached Home (2026) | Land Transfer Tax |

|---|---|---|

| Edmonton | ~$571,000 | $0 provincial |

| Toronto | $1.4M+ | $18,000–$30,000+ |

| Vancouver | $1.8M+ | $16,000–$32,000+ |

The Part Most People Miss About Buying in Alberta

Everyone knows Edmonton homes are cheaper. What people don’t always do is actually run the numbers on closing day.

Alberta has no provincial land transfer tax. On a $571,000 purchase, your land titles registration fee is around $622. An Ontario buyer buying the same house in Toronto would pay upward of $18,000 in provincial and municipal land transfer tax on top of everything else. That’s a real difference in cash you need at the table on day one.

Alberta also has no PST — only the federal 5% GST. Day-to-day costs are lower, and that affects how much of your income is actually available for a mortgage payment month to month. The math consistently favours Alberta for buyers coming from high-cost provinces, and it’s not marginal.

What to Make of Mortgage Rates in 2026

Rates aren’t where they were in 2020. They may not get back there. What actually matters is whether today’s payment is manageable and whether you pass the stress test, which requires qualifying at your contract rate plus 2%.

On a $571,000 purchase with 10% down, your insured mortgage would be around $520,000. At a five-year fixed rate in the 4.5–5% range on a 25-year amortization, monthly payments land somewhere in the $2,800–$3,000 range. Whether that works depends entirely on your income and what else you’re carrying.

On waiting for rates to drop — some buyers who held off through 2023 and 2024 did see relief. They also watched prices hold and inventory tighten. Rate cuts pull buyers back into the market fast, which puts upward pressure on prices. Waiting is not a neutral strategy. It trades one risk for another.

Who Edmonton Makes the Most Sense For Right Now

If you’re relocating from Ontario or BC, the math is pretty clear. The household income that qualifies you for a condo in Toronto qualifies you for a detached home in some of Edmonton’s best southwest communities. That’s not a small upgrade — it’s a fundamentally different standard of living for a similar monthly payment, plus no land transfer tax at closing.

If you’re a local first-time buyer, the conversation is more specific to your situation — income, down payment, what you can actually carry. Edmonton is more affordable than most Canadian cities, but $571,000 is still a real number that needs real preparation.

If you’re upgrading within Edmonton, current inventory gives you more to choose from than the 2022 seller’s market did. More selection means less pressure to overbid.

See What You Can Actually Afford in Edmonton

The Edmonton Buyer Profile walks through your purchasing power, neighbourhood matches, and total cash needed to close — in about four minutes.

Build Your Buyer ProfileBefore You Start Looking at Homes

Get pre-approved first. Not necessarily to lock in a rate, but to know exactly what you qualify for and what that payment actually looks like. It also means you can move quickly when you find the right place, which matters even in a more balanced market.

From there, get clear on what you need — bedrooms, neighbourhood, commute, schools if that applies. Edmonton is a big city with a wide range of communities at different price points. Knowing your priorities before you start saves a lot of time and avoids ending up in a home that technically fits the budget but not the life.

If you have questions about how the buying process works in Alberta — deposits, conditions, timelines — the buyers guide has a full breakdown of what to expect from offer to possession.

Frequently Asked Questions

Is 2026 a good time to buy a home in Edmonton?

For most buyers, yes. Edmonton is still one of the most affordable major cities in Canada at $571,372 average detached, and inventory is up from 2024 levels. That means more selection and more room to negotiate than during the peak seller’s market.

What is the average home price in Edmonton in 2026?

As of February 2026, the average detached home was $571,372. Entry-level detached in southwest communities like Glenridding and Keswick starts in the $550,000–$650,000 range. Luxury and infill in mature neighbourhoods like Windermere and Glenora average $1.6M–$1.7M.

Does Alberta have a land transfer tax?

No. Alberta has no provincial land transfer tax. You pay a land titles registration fee — on a $571,000 home, around $622. An Ontario buyer buying the same home in Toronto would pay over $18,000 in combined provincial and municipal land transfer tax.

How do Edmonton home prices compare to Toronto and Vancouver?

Edmonton’s average detached is around $571,000. Toronto benchmarks over $1.4 million. Vancouver is over $1.8 million. The income that qualifies you for a starter condo in Toronto qualifies you for a detached home in Edmonton’s best southwest neighbourhoods.

Should I wait for interest rates to drop before buying in Edmonton?

It depends on your situation. When rates drop, demand comes back fast and prices tend to follow. If Edmonton values rise while you wait, the savings from a lower rate can be offset by a higher purchase price. The real question is whether you can comfortably carry today’s payment.

What do I need to buy a home in Edmonton?

Minimum 5% down on homes under $500,000, or 5% on the first $500,000 and 10% on the remainder above that. You also need to qualify at your contract rate plus 2% for the stress test. Budget for closing costs: roughly $1,500 in legal fees, $575 for a home inspection, land titles fees, and moving costs.

Categories

Recent Posts