What a $600,000 Home in Edmonton Actually Costs Per Month

Homes with Tristan: Alberta Buyer Finance

What a $600,000 Home in Edmonton Actually Costs Per Month

By Tristan Boire, REALTOR | Park Realty, Sherwood Park AB

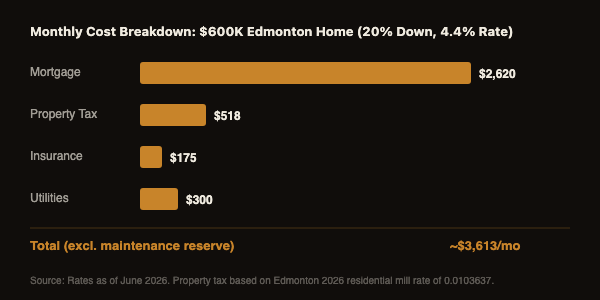

Here’s the number: a $600,000 home in Edmonton with 20% down is going to run you somewhere around $3,600–$3,700 per month all-in. That’s mortgage, property tax, home insurance, and utilities. Not a rough guess — we’re breaking it down line by line below.

Worth noting: $600K is basically the Edmonton detached average right now. According to the Realtors Association of Edmonton’s May 2026 stats, the GEA detached average came in at $604,744. So this isn’t some hypothetical — this is the market you’re actually buying into.

If you’re moving here from Ontario or BC, there’s also a financial advantage most people don’t fully appreciate until they run the numbers side by side. We’ll cover that too.

Key Takeaways

- → A $600K Edmonton home with 20% down costs roughly $3,613/month in recurring costs before any maintenance reserve.

- → Alberta has zero provincial land transfer tax — a saving of $9,200+ compared to Ontario buyers.

- → The stress test at 4.4% means qualifying at 6.4% — rough household income needed is $115K–$125K.

- → Budget an extra $500/month as a maintenance reserve — that’s the cost most first-time buyers forget.

What’s the Mortgage Payment on a $600K Home in Edmonton?

At 4.4% on a 5-year fixed — and the current range at major banks is 4.3%–4.5% as of June 2026 — a $480,000 mortgage (that’s 20% down on a $600K home) runs $2,620/month over a 25-year amortization. That’s your baseline.

But not everyone puts 20% down, so here’s how the three main scenarios shake out:

| Scenario | Down Payment | CMHC Premium | Monthly Payment |

|---|---|---|---|

| 20% down | $120,000 | None | $2,620/mo |

| 10% down | $60,000 | $16,740 (3.10%) | $3,040/mo |

| 5% down | $30,000 | $22,800 (4.00%) | $3,240/mo |

One thing that trips people up on CMHC: the insurance premium doesn’t come out of your pocket at closing as a separate charge. It gets added to the mortgage balance and amortized over the full 25 years. So with 10% down, you’re not paying $16,740 upfront — it just raises your insured mortgage from $540,000 to $556,740, and your monthly payment reflects that.

The gap between 5% down and 20% down is about $620/month. Over five years, that’s roughly $37,000 more in mortgage payments. Whether that math works depends on how long it would take you to save the extra down payment and what you’d do with those funds in the meantime.

What About Property Tax, Insurance, and Utilities?

Beyond the mortgage, a $600K Edmonton home adds roughly $900–$1,000 per month in property tax, home insurance, and utilities. Here’s how each breaks down.

Property tax: Edmonton’s 2026 residential mill rate is 0.0103637. On a $600,000 assessed value, that works out to $6,218/year — approximately $518/month. Property taxes are assessed on the full property value, so if the city assesses your home above or below $600K, your bill adjusts accordingly. The current rate is published each spring at edmonton.ca.

Home insurance: For a detached home in Edmonton, budget $150–$200 per month. A reasonable working number is $175/month. Your actual premium depends on the home’s age, construction type, and your claims history — older homes tend to run higher. Shop at least two or three providers before settling.

Utilities: Edmonton winters are real, and gas heat runs high from October through April. Based on EPCOR’s current rate of about 12 cents per kWh, electricity for a detached home runs $150–$170/month. Natural gas (ATCO) averages $100–$130/month across the year, though winter months can run considerably higher. Water, sewer, and waste collection add roughly $80–$100/month. Combined, budget $300–$350/month — lean toward the higher end in your first Edmonton winter if you’re coming from a milder climate.

How Does Alberta Compare to Ontario on Upfront Costs?

Alberta buyers pay zero provincial land transfer tax. Ontario buyers pay $9,200+ on a $600,000 purchase. If you’re buying in Toronto specifically, add the City of Toronto’s municipal land transfer tax on top — another $9,200 roughly — for a combined hit of $18,400+ that you simply do not pay in Alberta.

That’s not a rounding error. That’s a full year of mortgage payments handed back to you on day one just by buying here instead of there.

Alberta also has no provincial sales tax. There’s 5% GST on new construction and certain services, but no PST stacked on top. If you’re coming from BC (7% PST) or Ontario (13% HST), the difference on home-related purchases and services adds up quickly.

One thing worth clarifying since I’ve heard it misquoted: Alberta does have provincial income tax. What it doesn’t have is a provincial sales tax. Those are different things. If you’re running financial projections for a move here, factor in Alberta’s income tax rates rather than assuming there are none.

For a full breakdown of what the move from Ontario actually costs and saves, the Moving to Edmonton guide covers it in detail.

What Income Do You Need to Qualify for a $600K Home?

With a contract rate of 4.4%, the stress test requires you to qualify at 6.4% (that’s your rate plus 2%, and it’s higher than the 5.25% floor, so 6.4% applies). In rough terms, that means you need to show you can carry the payment at a rate considerably higher than what you’ll actually pay.

For a $480,000 mortgage with 20% down, a household income in the range of $115,000–$125,000 is typically where lenders start getting comfortable. That number shifts based on your existing debts — car payments, student loans, credit card balances — because lenders look at your total debt service ratio, not just the mortgage in isolation.

The stress test exists to ensure you can still carry the mortgage if rates rise after your term renews. At 6.4%, lenders want to see that your housing costs (mortgage, property tax, heating) plus your other debt payments don’t exceed a certain percentage of your gross income. Most lenders use 39% for the GDS (gross debt service) ratio and 44% for TDS (total debt service) — these are OSFI’s B-20 guideline limits, which remain in effect for 2026.

If you want a precise qualification number for your situation, talk to a mortgage broker — not just your bank. A broker has access to multiple lenders and can often find better options than walking into your branch. The buyers page has contact info for three brokers I work with regularly in Edmonton.

What’s the Maintenance Budget Nobody Talks About?

Budget 1% of the home’s value per year for maintenance and repairs. On a $600K home, that’s $6,000 annually — or $500/month set aside as a reserve. It’s not a guaranteed expense, but it’s a real one.

This is the number that catches a lot of first-time buyers off guard. They budget the mortgage, they know the property taxes, and then year two arrives with a furnace replacement or a roof that needs attention and it’s a $6,000–$12,000 surprise. The 1% rule doesn’t mean you’ll spend that every single year — some years it’s zero, others it’s more — but it averages out over time.

New builds tend to run lower in the first five years. Most major systems are under warranty and the builder is still on the hook for deficiencies. Older homes in established neighbourhoods can run higher — especially if a home inspection flags deferred maintenance items that weren’t addressed before listing.

When I work with buyers, I always flag the inspection report items that aren’t deal-breakers but will cost money in the next one to three years. A water heater that’s 12 years old isn’t an immediate problem, but it’s going in that maintenance reserve calculation. It changes how you think about the total cost of owning a specific home, not just any home at this price point.

Add that $500/month reserve to the $3,613 in recurring costs and you’re looking at roughly $4,113/month as a realistic all-in budget for a $600K Edmonton home with 20% down. That’s the number worth stress-testing against your income before making an offer.

Ready to Run Your Numbers?

Get the Free Edmonton Buyer’s Guide

Every step, every cost, every timeline. Written for people buying in Edmonton. Free download.

Get the GuideCommon Questions

Can I buy a $600K home in Edmonton on a single income?

Yes, it’s possible — but you’d need a strong single income. Qualifying at the stress test rate of 6.4% on a $480K mortgage (20% down scenario) generally requires a gross income of around $115K–$125K with minimal other debt. If you carry a car payment or student loans, that bar moves higher. A mortgage broker can run your specific numbers before you start shopping.

Is it better to put 20% down or keep more cash?

20% down avoids CMHC insurance and lowers your monthly payment by $420–$620 depending on the scenario. But keeping cash has value too — especially for a maintenance reserve, emergency fund, or investment account. The right answer depends on your full financial picture. I’d rather you put 10% down and keep $30K liquid than stretch to 20% and be cash-poor in year one. Talk to both a broker and a financial advisor before deciding.

What are closing costs on a $600K Edmonton home?

In Alberta, you’re looking at roughly $3,000–$5,000 in closing costs on a $600K purchase. That typically breaks down as: legal fees ($1,500–$2,000), home inspection ($500–$650), and title insurance ($300–$400). There is no provincial land transfer tax in Alberta, which keeps this number dramatically lower than it would be in Ontario. Budget 1%–1.5% of the purchase price as a safe estimate and you won’t be caught short.

How does CMHC mortgage insurance work in Alberta?

CMHC mortgage insurance is required any time your down payment is less than 20% of the purchase price. It protects the lender (not you) in the event of default. The premium is calculated as a percentage of the total mortgage — 4.00% at 5% down, 3.10% at 10% down, 2.80% at 15% down. The premium gets added to your mortgage balance rather than paid upfront, so it’s baked into your monthly payment over the full amortization period. Alberta does not charge PST on the CMHC premium (some provinces do).

Categories

Recent Posts